2026 Student Loan Reforms: Save 5% Annually with New Policies

Anúncios

Understanding the Latest 2026 Student Loan Reforms: What Every Borrower Needs to Know to Save 5% Annually

The landscape of student loan repayment is constantly evolving, and for millions of borrowers, understanding these changes is crucial to financial well-being. As we approach 2026, significant 2026 Student Loan Reforms are on the horizon, promising to reshape how individuals manage their educational debt. These reforms are not merely administrative tweaks; they represent a concerted effort to alleviate the burden of student loans, with the potential to help borrowers save an impressive 5% annually on their payments. This comprehensive guide will delve into the intricacies of these upcoming changes, providing you with the knowledge and strategies necessary to navigate the new system, optimize your repayments, and ultimately, enhance your financial stability.

Anúncios

Student loan debt has long been a pressing issue for individuals and the economy at large. The sheer volume of outstanding debt has prompted policymakers to seek innovative solutions, leading to the development of these anticipated 2026 Student Loan Reforms. Our aim is to break down the complexities, making these vital updates accessible and actionable for every borrower. Whether you are currently in repayment, nearing graduation, or still in school, these reforms will undoubtedly impact your financial future. By understanding them now, you can proactively plan and position yourself to reap the maximum benefits.

The Genesis of the 2026 Student Loan Reforms: Why Now?

The journey towards the 2026 Student Loan Reforms has been a long one, driven by a growing recognition of the challenges faced by student loan borrowers. For decades, the cost of higher education has steadily risen, often outpacing inflation and wage growth. This has led to an escalating student debt crisis, with millions of Americans struggling to make their monthly payments, deferring life milestones, and facing significant financial stress. The existing repayment systems, while offering some flexibility, often proved insufficient for many, particularly those in lower-paying jobs or experiencing economic hardship.

Policymakers, economists, and advocacy groups have consistently highlighted the need for more robust and equitable solutions. The COVID-19 pandemic further exacerbated these issues, bringing into sharp focus the fragility of many borrowers’ financial situations and prompting temporary relief measures. These experiences underscored the necessity of a more permanent and sustainable framework for student loan management. The 2026 Student Loan Reforms are a direct response to these pressures, aiming to create a more manageable and fair system that supports both individual borrowers and the broader economy. The reforms are built upon extensive research, public feedback, and a desire to foster economic mobility rather than hinder it.

Anúncios

The primary goals behind these reforms include:

- Reducing Repayment Burden: Making monthly payments more affordable and predictable for a wider range of borrowers.

- Simplifying the System: Streamlining the often-confusing array of repayment plans and options.

- Promoting Financial Stability: Helping borrowers avoid default and achieve long-term financial health.

- Addressing Equity Concerns: Ensuring that the reforms benefit those who need assistance the most, particularly low and middle-income individuals.

- Stimulating Economic Growth: Freeing up disposable income for borrowers, which can then be used for other investments, consumption, and savings.

Understanding these underlying motivations is key to appreciating the scope and potential impact of the 2026 Student Loan Reforms. They are designed not just to fix immediate problems but to build a more resilient and supportive framework for future generations of students.

Key Provisions of the 2026 Student Loan Reforms: A Detailed Breakdown

The heart of the 2026 Student Loan Reforms lies in their specific provisions. While the final details may be subject to minor adjustments as they are implemented, the core tenets are expected to remain consistent. Here, we’ll break down the most impactful changes, particularly those that contribute to the potential 5% annual savings for borrowers.

Revised Income-Driven Repayment (IDR) Plans

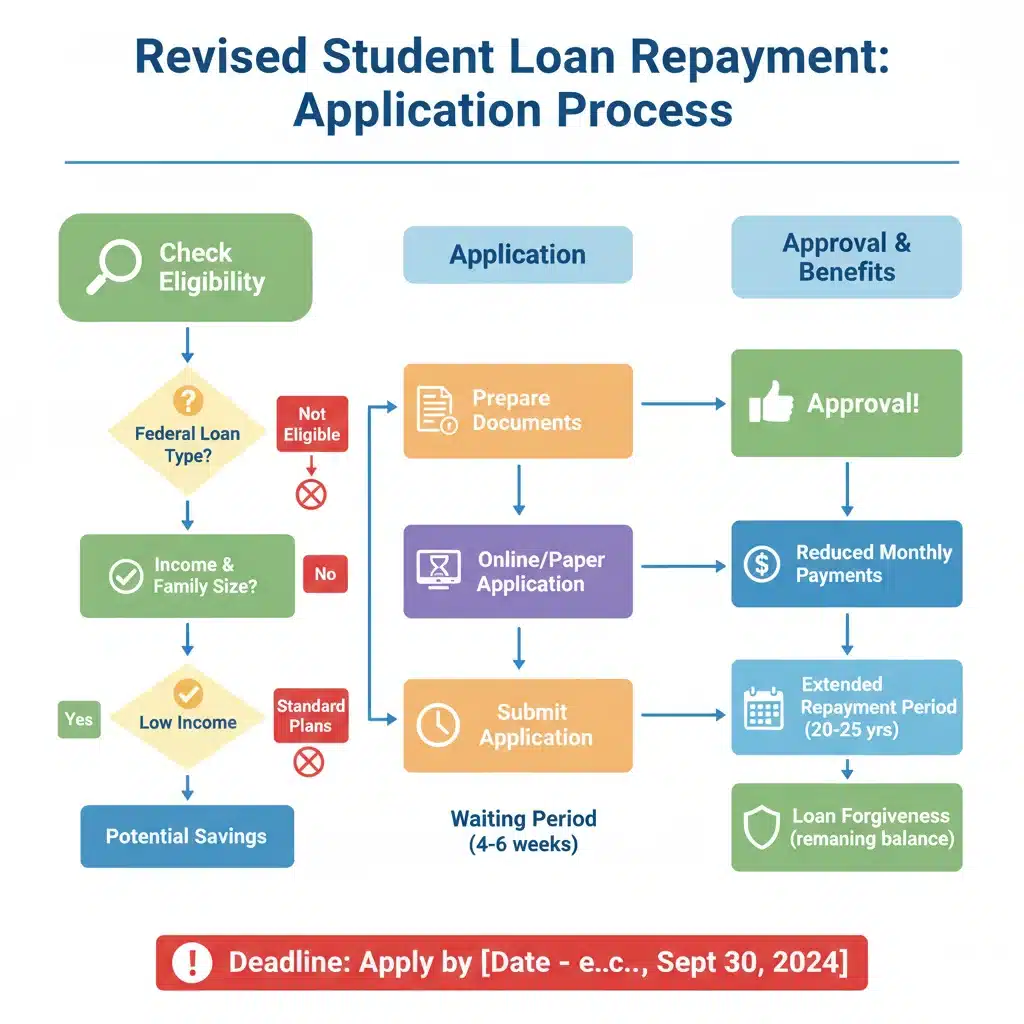

One of the most significant changes involves the overhaul of existing Income-Driven Repayment (IDR) plans. These plans are designed to make monthly payments affordable by basing them on a borrower’s income and family size. The 2026 Student Loan Reforms are expected to introduce a new, more generous IDR plan, or significantly modify existing ones, with several key improvements:

- Lower Discretionary Income Calculation: The percentage of discretionary income used to calculate monthly payments is expected to decrease. Currently, some IDR plans calculate payments based on 10% of discretionary income. The reforms may reduce this to 5% for undergraduate loans, making monthly payments significantly lower. This is a primary driver of the potential 5% annual savings.

- Increased Income Exemption: The amount of income protected from payment calculations (i.e., not considered discretionary) is likely to increase. This means a larger portion of a borrower’s income will be exempt, further reducing their monthly payment obligation.

- Shorter Repayment Periods for Smaller Balances: For borrowers with smaller loan balances, the reforms may introduce shorter repayment periods before loan forgiveness. This accelerates the path to debt relief for a substantial number of individuals.

- Interest Subsidies: A crucial aspect of the new reforms is the potential for significant interest subsidies. Under current IDR plans, unpaid interest can capitalize, causing the loan balance to grow even while making payments. The 2026 Student Loan Reforms aim to prevent this by ensuring that if a borrower’s monthly payment doesn’t cover the interest, the government will cover the remaining interest, preventing the loan balance from increasing as long as payments are made. This is a game-changer for many, preventing the demoralizing experience of seeing debt grow despite regular payments.

Simplified Application and Enrollment Process

Historically, enrolling in and recertifying for IDR plans has been a cumbersome process, leading to many borrowers missing out on benefits. The 2026 Student Loan Reforms are expected to simplify this significantly:

- Automatic Enrollment: Efforts may be made to automatically enroll eligible borrowers into the most beneficial IDR plan, or at least to make the application process much more straightforward and less prone to errors.

- Streamlined Annual Recertification: The annual recertification process, which often requires submitting income documentation, is expected to become more seamless, potentially through data sharing agreements with the IRS, reducing the administrative burden on borrowers.

Changes to Public Service Loan Forgiveness (PSLF)

While not a direct component of the IDR changes, the 2026 Student Loan Reforms may also bring refinements to the Public Service Loan Forgiveness (PSLF) program. PSLF forgives the remaining balance on Direct Loans after 120 qualifying monthly payments made under a qualifying repayment plan while working full-time for a qualifying employer. Potential changes could include:

- Broader Definition of Qualifying Employment: Expanding the types of public service that qualify for PSLF.

- Easier Payment Tracking: Improving the system for tracking qualifying payments, reducing confusion and errors that have plagued the program in the past.

These detailed provisions illustrate the depth of the upcoming changes. Each element is designed to work in concert to create a more supportive environment for student loan borrowers, ultimately leading to tangible financial relief.

How to Maximize Your Savings: Strategies for the 2026 Student Loan Reforms

The promise of saving up to 5% annually on your student loan payments through the 2026 Student Loan Reforms is exciting, but realizing these savings requires proactive engagement. Here are actionable strategies to help you maximize the benefits of the new policies:

1. Understand Your Loan Types and Current Repayment Plan

Before you can leverage the reforms, you need to know what kind of loans you have. Federal student loans (Direct Loans, FFEL Program loans, Perkins Loans) are generally eligible for IDR plans and PSLF. Private student loans are not. Identify whether your loans are federal or private, and if federal, which specific types. Also, review your current repayment plan. Are you on a Standard Repayment Plan, an Extended Plan, or an existing IDR plan? Knowing this will help you determine the best path forward under the new 2026 Student Loan Reforms.

2. Monitor Official Announcements and Updates

The specifics of the 2026 Student Loan Reforms will be rolled out gradually. Stay informed by regularly checking official sources such as the U.S. Department of Education’s Federal Student Aid (FSA) website, and reputable financial news outlets. Sign up for email updates from your loan servicer and the FSA. This will ensure you have the most accurate and up-to-date information on eligibility requirements, application deadlines, and implementation timelines.

3. Re-evaluate Your Income and Family Size

Since the new IDR plans under the 2026 Student Loan Reforms will heavily rely on your income and family size, it’s crucial to have this information readily available and up-to-date. If your income has decreased, or your family size has increased, your monthly payments could be significantly lower. Be prepared to provide accurate documentation when applying or recertifying.

4. Consider Consolidating Your Loans

Some older federal loans (like certain FFEL Program loans or Perkins Loans) may not directly qualify for the most beneficial new IDR plans unless they are consolidated into a Direct Consolidation Loan. If you have these types of loans, investigate whether consolidation would make you eligible for the improved IDR options under the 2026 Student Loan Reforms. Be aware that consolidation can sometimes reset your payment count for PSLF, so weigh the pros and cons carefully if PSLF is a goal.

5. Apply for the New IDR Plan When Available

Once the new IDR plan is officially launched and applications open, apply as soon as you are eligible. Don’t wait. The sooner you transition to a more favorable plan, the sooner you can start realizing the 5% annual savings. Pay close attention to the application process, ensuring all required documentation is submitted correctly to avoid delays.

6. Understand the Interest Subsidies

A key benefit of the 2026 Student Loan Reforms is the prevention of interest capitalization under the new IDR plan. Ensure you understand how this works. If your payment is less than the accrued interest, the government will cover the difference, preventing your loan balance from growing. This feature alone can lead to substantial long-term savings and provide significant peace of mind.

7. Re-evaluate PSLF Eligibility (If Applicable)

If you work in public service, closely examine any changes to PSLF under the 2026 Student Loan Reforms. Even if you previously thought you weren’t eligible or had issues with qualifying payments, the reforms might open new avenues for forgiveness. Confirm your employer’s eligibility and ensure your payments are properly tracked.

8. Seek Professional Guidance If Needed

The world of student loans can be complex. If you find yourself overwhelmed or unsure about how the 2026 Student Loan Reforms apply to your specific situation, consider seeking advice from a reputable non-profit credit counselor or a financial advisor specializing in student debt. Be wary of companies that charge high fees for services you can often get for free from the Department of Education.

By proactively implementing these strategies, you can position yourself to fully benefit from the 2026 Student Loan Reforms and take a significant step towards alleviating your student loan burden.

Potential Challenges and Considerations with the 2026 Student Loan Reforms

While the 2026 Student Loan Reforms offer a beacon of hope for many borrowers, it’s also important to consider potential challenges and nuances in their implementation and impact. No large-scale policy change is without its complexities, and being aware of these can help you better navigate the new landscape.

1. Implementation Delays and Technical Glitches

Historically, major changes to federal student loan programs have sometimes faced implementation challenges. The sheer scale of the 2026 Student Loan Reforms means that there could be initial delays, technical glitches with new application portals, or confusion among loan servicers. Borrowers should be patient but persistent, keeping detailed records of all communications and applications. Staying informed through official channels will be crucial to overcoming any initial hurdles.

2. Communication and Awareness

For the 2026 Student Loan Reforms to be truly effective, borrowers need to be aware of them and understand how to access the benefits. There’s a risk that some borrowers, particularly those who are disengaged from their loan management, might miss out on these opportunities. This underscores the importance of public education campaigns and the role of resources like this article in spreading awareness.

3. Impact on Different Borrower Groups

While the reforms aim to benefit a broad spectrum of borrowers, their impact may vary. For example, borrowers with very high incomes relative to their debt might see less dramatic reductions in payments compared to those with lower incomes. Additionally, borrowers with only private loans will not directly benefit from these federal reforms. It’s essential for each borrower to assess how the new rules apply to their unique financial situation.

4. Long-Term Fiscal Sustainability

The generosity of the 2026 Student Loan Reforms, particularly the enhanced interest subsidies and lower discretionary income calculations, will come at a significant cost to taxpayers. While the immediate benefit to borrowers is clear, there will likely be ongoing debates about the long-term fiscal sustainability of these programs. This political dimension could influence future adjustments to the reforms, making it important to remain vigilant.

5. Need for Continued Advocacy

Even with substantial reforms, the student loan system will likely continue to evolve. Advocacy for further improvements, simplification, and equitable access will remain necessary. Borrowers and their supporters should continue to engage with policymakers to ensure the system remains responsive to the needs of students and graduates.

Acknowledging these potential challenges doesn’t diminish the positive intent or potential impact of the 2026 Student Loan Reforms. Instead, it equips borrowers with a more realistic understanding and encourages a proactive approach to navigating the new system effectively.

Beyond 2026: The Future of Student Loan Repayment

The 2026 Student Loan Reforms are a significant milestone, but they are unlikely to be the final word on student debt. The nature of higher education financing and its impact on individuals and the economy means that the discussion and potential for further changes will continue. Understanding this broader context can help borrowers prepare for an evolving financial landscape.

Ongoing Evolution of IDR Plans

While the new IDR plan under the 2026 Student Loan Reforms is designed to be more beneficial, the parameters of these plans have historically been subject to adjustments based on economic conditions, political priorities, and program efficacy. Borrowers should anticipate that future administrations or legislative bodies might refine these plans further. This underscores the importance of continuous monitoring and adapting your repayment strategy as needed.

Focus on Prevention: Addressing the Root Causes of Debt

Beyond repayment reforms, there’s a growing recognition that addressing the root causes of student debt is equally vital. This includes discussions around:

- Affordability of Higher Education: Policies aimed at controlling tuition costs, increasing state funding for public institutions, and expanding grant aid.

- Accountability for Institutions: Holding colleges and universities more accountable for student outcomes, particularly regarding graduate employment and earnings relative to tuition costs.

- Financial Literacy: Enhancing financial education for prospective students to help them make informed decisions about borrowing and repayment.

While these are separate from the 2026 Student Loan Reforms, they represent the broader ecosystem of student finance that will continue to influence future policies.

Technological Advancements in Loan Management

Expect to see further integration of technology in student loan management. This could include AI-powered tools to help borrowers choose the best repayment plans, more sophisticated online portals, and seamless data sharing for income verification. These advancements aim to make the process less burdensome and more efficient for borrowers.

The Role of Private Lenders

The 2026 Student Loan Reforms primarily focus on federal loans. However, the private student loan market also continues to play a significant role. While federal reforms don’t directly impact private loans, a more stable federal system might indirectly influence private lenders to offer more competitive terms or flexible repayment options to attract borrowers. It’s crucial to understand the distinction between federal and private loans and to explore options specific to private debt if applicable.

Preparing for the Long Term

For borrowers, the key takeaway is that managing student debt is a marathon, not a sprint. The 2026 Student Loan Reforms offer powerful tools to help you along the way, but a comprehensive financial plan that includes budgeting, saving, and investing remains essential. Regularly review your financial situation, understand how policy changes affect you, and adapt your strategies to ensure long-term financial health.

The future of student loan repayment is dynamic. By staying informed, being proactive, and leveraging the opportunities presented by the 2026 Student Loan Reforms, borrowers can navigate this journey successfully and achieve greater financial freedom.

Conclusion: Embracing the Future with the 2026 Student Loan Reforms

The upcoming 2026 Student Loan Reforms represent a pivotal moment for millions of student loan borrowers across the nation. With the potential to save up to 5% annually on loan payments, these changes are designed to offer substantial relief, foster financial stability, and pave a clearer path towards debt freedom. From revised Income-Driven Repayment plans with lower discretionary income calculations and robust interest subsidies to streamlined application processes and potential refinements to PSLF, the reforms aim to create a more equitable and manageable system.

However, realizing these benefits is not automatic. It requires a proactive approach: understanding your current loan portfolio, staying informed through official channels, re-evaluating your financial situation, and strategically applying for the new programs as they become available. While potential challenges such as implementation complexities and the need for ongoing advocacy exist, the overall thrust of these reforms is overwhelmingly positive.

As we move towards 2026 and beyond, the landscape of student loan repayment will continue to evolve. By embracing the opportunities presented by these reforms, staying vigilant about future policy changes, and maintaining a solid personal financial strategy, borrowers can confidently navigate their educational debt. The 2026 Student Loan Reforms are more than just new rules; they are an invitation to take control of your financial future and transform the burden of student debt into a manageable step on your journey to prosperity. Start preparing today to ensure you are well-positioned to benefit fully from these transformative changes.