Affordable Care Act 2026: New Subsidies Could Reduce Your Premiums by up to 25%

Anúncios

Affordable Care Act 2026: New Subsidies Could Reduce Your Premiums by up to 25%

For millions of Americans, the cost of healthcare has long been a significant burden. Navigating the complexities of health insurance, understanding deductibles, co-pays, and monthly premiums can feel like an insurmountable challenge. However, a glimmer of hope is on the horizon with the upcoming changes to the Affordable Care Act (ACA) in 2026. These updates, particularly the introduction of new and enhanced subsidies, are poised to make health insurance more accessible and affordable than ever before, potentially reducing your monthly premiums by up to an astonishing 25%.

Anúncios

The ACA, often referred to as Obamacare, was signed into law in 2010 with the ambitious goal of expanding health insurance coverage to uninsured Americans and reducing the rising costs of healthcare. Over the years, it has undergone various modifications and challenges, but its core mission remains. The 2026 enhancements represent a pivotal moment, reaffirming the commitment to affordable healthcare and offering substantial financial relief to individuals and families struggling to keep up with premium costs. Understanding these changes is crucial for anyone seeking to minimize their healthcare expenses and ensure they have adequate coverage.

This comprehensive guide will delve deep into the specifics of the ACA 2026 subsidies, explaining who is eligible, how these subsidies are calculated, and what steps you can take to maximize your savings. We will explore the historical context of the ACA, the recent legislative actions that paved the way for these changes, and the broader impact on the American healthcare landscape. By the end of this article, you will have a clear understanding of how the ACA 2026 subsidies can directly benefit you, empowering you to make informed decisions about your health insurance future.

Anúncios

The Evolution of the ACA: A Brief History and the Path to 2026

To fully appreciate the significance of the ACA 2026 subsidies, it’s helpful to understand the journey of the Affordable Care Act itself. When it was first enacted, the ACA introduced several key provisions aimed at reforming the health insurance market. These included the establishment of health insurance marketplaces (exchanges), where individuals and small businesses could shop for plans; the mandate for most Americans to have health insurance or pay a penalty (though this penalty was later repealed); and the expansion of Medicaid eligibility in many states. Crucially, the ACA also introduced premium tax credits and cost-sharing reductions to help make coverage more affordable for low- and middle-income individuals.

However, the initial rollout and subsequent years saw continuous debate and legislative attempts to modify or repeal the law. Despite these challenges, the ACA has remained a cornerstone of American healthcare policy. One of the most impactful developments leading to the 2026 changes was the American Rescue Plan Act of 2021. This landmark legislation temporarily expanded ACA subsidies, making them more generous and available to a wider range of income levels. Specifically, it eliminated the income cap for subsidy eligibility (previously 400% of the federal poverty level, or FPL) and ensured that no one would pay more than 8.5% of their household income for a benchmark plan on the marketplace.

These enhanced subsidies proved incredibly successful in reducing premiums and increasing enrollment. Recognizing their positive impact, Congress extended these provisions through the Inflation Reduction Act of 2022, ensuring their continuation through 2025. The discussions and legislative efforts now point towards a permanent extension or further enhancement of these subsidies for 2026 and beyond. This commitment reflects a growing understanding of the vital role these financial aids play in ensuring access to healthcare for millions of Americans. The ACA 2026 subsidies are not just a continuation but a potential refinement of these successful policies, aiming for even broader impact and affordability.

Understanding the New ACA 2026 Subsidies: What’s Changing?

The core of the excitement surrounding the ACA 2026 changes lies in the proposed enhancements to premium tax credits. While the exact legislative language is still being finalized, the prevailing sentiment and current proposals suggest a continued commitment to the expanded subsidies introduced by the American Rescue Plan Act and extended by the Inflation Reduction Act. This means:

- Elimination of the Income Cliff: Previously, individuals earning more than 400% of the FPL were ineligible for any subsidies, leading to a sudden and significant increase in premium costs for those just above the threshold. The new framework aims to eliminate this cliff, ensuring that everyone pays no more than a certain percentage of their income for a benchmark plan, regardless of how high their income is.

- Increased Generosity for All Income Levels: For those already eligible for subsidies, the new structure means even lower out-of-pocket premium costs. The percentage of income individuals are expected to contribute towards premiums will be further reduced across various income brackets, making health insurance significantly more affordable.

- Broader Eligibility: By eliminating the income cap and increasing generosity, more individuals and families who previously found marketplace plans unaffordable will now qualify for substantial financial assistance. This expands the safety net, drawing more people into covered healthcare.

These changes are projected to reduce premiums by up to 25% for many individuals. This isn’t a blanket reduction for everyone, but rather a significant potential saving for those who qualify for and utilize the enhanced subsidies. For example, a family of four earning 300% of the FPL might see their monthly premium decrease substantially, transforming an otherwise prohibitive cost into something manageable. The impact is particularly profound for middle-income earners who often struggled with the high cost of unsubsidized plans but were previously just above the eligibility threshold for assistance.

It’s important to remember that the exact percentage of savings will depend on several factors, including your household income, family size, the cost of benchmark plans in your area, and the specific plan you choose. However, the overarching goal of the ACA 2026 subsidies is to ensure that a greater proportion of your income remains available for other essential needs, rather than being consumed by health insurance premiums.

Who Qualifies for ACA 2026 Subsidies?

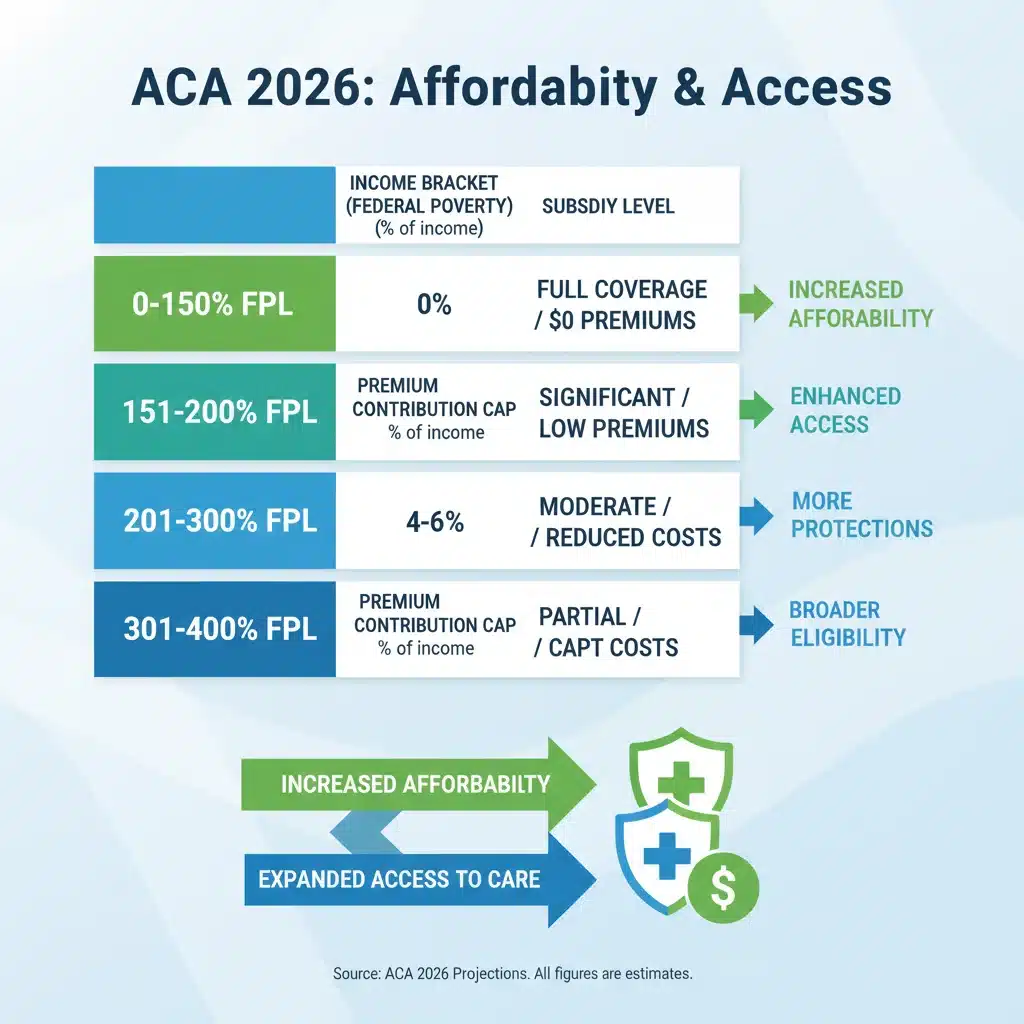

Eligibility for ACA 2026 subsidies primarily revolves around your household income relative to the Federal Poverty Level (FPL) and your access to other affordable health coverage. While the exact FPL figures are updated annually, the general principles of eligibility remain consistent. Here’s a breakdown:

Income-Based Eligibility

- Below 100% FPL: In states that have expanded Medicaid, individuals and families below 138% FPL are typically eligible for Medicaid. In non-expansion states, those below 100% FPL might fall into the "coverage gap" and not qualify for marketplace subsidies, though this is a critical area of ongoing debate and potential future reforms.

- 100% to 150% FPL: Individuals and families in this income bracket will likely qualify for the most generous subsidies, potentially paying very little or even nothing for a benchmark silver plan. The goal is to ensure premiums are effectively minimal.

- 150% to 400% FPL: Significant subsidies will continue to be available in this range, ensuring that benchmark plan premiums remain a low percentage of household income.

- Above 400% FPL: This is where the elimination of the income cliff becomes most impactful. Even if your income is above 400% FPL, you will still be eligible for subsidies if the cost of a benchmark silver plan would exceed 8.5% of your household income. This ensures that no one is priced out of coverage due to high premiums in their area.

Other Eligibility Factors

- No Access to Affordable Employer-Sponsored Coverage: You generally won’t qualify for ACA subsidies if you have access to affordable health insurance through your employer or your spouse’s employer. "Affordable" is defined by specific government thresholds (e.g., the employee’s share of the premium for self-only coverage must be less than a certain percentage of household income).

- Lawful Presence in the U.S.: You must be a U.S. citizen or lawfully present immigrant to be eligible for subsidies.

- Not Incarcerated: Individuals who are incarcerated are not eligible for marketplace plans or subsidies.

It’s crucial to use the official HealthCare.gov website or your state’s marketplace to determine your precise eligibility. These platforms have tools that calculate your estimated subsidies based on your projected income and household information. The ACA 2026 subsidies are designed to be dynamic, adjusting to your financial situation to provide the maximum possible relief.

Maximizing Your Savings: How to Apply for ACA 2026 Subsidies

Applying for ACA subsidies is a straightforward process, primarily conducted through the official health insurance marketplaces. Here’s a step-by-step guide to ensure you maximize your potential savings:

1. Gather Your Information

Before you begin, have the following information ready for all members of your household:

- Income Information: This includes W-2s, pay stubs, self-employment income records, Social Security benefits, unemployment benefits, and any other sources of income. You’ll need to estimate your modified adjusted gross income (MAGI) for the year you want coverage. Accurate income projection is vital for correct subsidy determination.

- Household Size: The number of people in your tax household, including yourself, your spouse, and any dependents you claim on your tax return.

- Social Security Numbers: For all household members applying for coverage.

- Immigration Documents: If applicable, for lawfully present immigrants.

- Current Health Insurance Information: If you have existing coverage, details about your plan.

2. Visit the Official Marketplace

Go to HealthCare.gov if your state uses the federal marketplace, or your state’s specific health insurance exchange website (e.g., Covered California, NY State of Health). Create an account if you don’t already have one.

3. Complete the Application

The application will ask for your personal details, household information, and crucially, your estimated household income for the upcoming year. Be as accurate as possible with your income projection. The marketplace will use this information to determine your eligibility for ACA 2026 subsidies and other financial assistance.

4. Review Your Eligibility and Plan Options

Once you submit your application, the marketplace will immediately inform you of your eligibility for premium tax credits (subsidies) and potentially cost-sharing reductions. It will then display various health plans available in your area, with the estimated monthly premium after your subsidies are applied. You’ll be able to compare plans based on cost, benefits, deductibles, and provider networks.

5. Choose a Plan and Enroll

Select the plan that best fits your healthcare needs and budget. The subsidies will be paid directly to your insurance company, reducing your monthly premium payment. You only pay the remaining balance.

6. Report Life Changes

It is critically important to report any changes in your income, household size, or eligibility for employer-sponsored coverage to the marketplace as soon as they occur. Failure to do so could result in incorrect subsidy amounts, leading to unexpected tax liabilities or missed savings. The ACA 2026 subsidies are designed to adapt, but only if you provide updated information.

The Impact of ACA 2026 Subsidies on the Healthcare Landscape

The extended and enhanced ACA 2026 subsidies are not just about individual savings; they have a far-reaching impact on the broader healthcare landscape:

- Increased Coverage Rates: By making health insurance more affordable, these subsidies are expected to significantly increase the number of insured Americans. This leads to a healthier population, as people are more likely to seek preventive care and necessary medical treatments when they have coverage.

- Reduced Uncompensated Care: With more people insured, hospitals and healthcare providers will see a reduction in uncompensated care, which is the cost of services provided to patients who are unable to pay. This can lead to greater financial stability for healthcare systems.

- Improved Health Outcomes: Access to insurance is directly linked to better health outcomes. Regular check-ups, early detection of diseases, and consistent management of chronic conditions become more feasible when cost is less of a barrier.

- Economic Benefits: A healthier workforce is a more productive workforce. Reduced healthcare costs for individuals can also free up disposable income, stimulating local economies.

- Stabilization of the Individual Market: By bringing more healthy individuals into the marketplace, the risk pool becomes larger and more balanced. This can help stabilize premiums overall, making the individual insurance market more robust and sustainable in the long term.

The commitment to these substantial subsidies through ACA 2026 subsidies signals a policy direction focused on universal access and affordability, aiming to mitigate the financial strain that healthcare costs impose on millions of families.

Potential Challenges and Future Outlook

While the prospect of enhanced ACA 2026 subsidies is overwhelmingly positive, it’s also important to acknowledge potential challenges and the ongoing political dynamics that influence healthcare policy. The permanence of these subsidies, while strongly supported by current legislative efforts, is always subject to future political shifts. Advocates for affordable healthcare will continue to push for legislative stability and further enhancements to ensure long-term access.

Another area of focus will be outreach and education. Even with generous subsidies, many eligible individuals may not be aware of their options or how to navigate the marketplace. Continued investment in consumer assistance programs, navigators, and public awareness campaigns will be crucial to ensure that everyone who qualifies for ACA 2026 subsidies can successfully enroll and benefit from them.

Furthermore, the ACA’s impact is not uniform across all states. Those states that have not expanded Medicaid still leave a significant portion of their low-income population without an affordable coverage option. Future reforms may continue to address this "coverage gap" to ensure a more equitable healthcare landscape nationwide.

Despite these challenges, the overall trajectory points towards a more accessible and affordable healthcare system. The sustained commitment to robust subsidies under the ACA 2026 framework represents a significant step forward in ensuring that quality health insurance is not a luxury, but a fundamental right for all Americans.

Case Studies: Real-World Impact of Enhanced Subsidies

To illustrate the tangible benefits of the ACA 2026 subsidies, let’s consider a few hypothetical scenarios based on the expected framework:

Case Study 1: The Young Professional

Sarah, a 28-year-old freelance graphic designer, earns $40,000 annually (approximately 300% of the FPL for a single individual). In previous years, without significant subsidies, a benchmark plan might have cost her upwards of $400-$500 per month, making it a considerable strain on her budget. With the enhanced ACA 2026 subsidies, her premium for a similar benchmark plan could drop to as low as $100-$150 per month, representing a 60-70% reduction. This saving allows her to invest more in her business and maintain a healthier financial life.

Case Study 2: The Middle-Income Family

The Rodriguez family, a couple with two children, earns $100,000 annually (approximately 350% of the FPL for a family of four). Before the enhanced subsidies, they might have faced monthly premiums of $1,200-$1,500, a significant portion of their income. Under the ACA 2026 framework, their benchmark plan premium could be capped at around 8.5% of their income, potentially bringing their monthly cost down to $700-$800. This 40-50% reduction frees up hundreds of dollars each month, which they can use for their children’s education or other household expenses.

Case Study 3: The Small Business Owner

Mark, a 55-year-old small business owner, earns $65,000 annually (approximately 450% of the FPL for a single individual). In the past, he would have been just over the 400% FPL subsidy cliff, facing full, unsubsidized premiums of $600-$800 per month. With the elimination of the income cliff in ACA 2026, if a benchmark plan in his area costs $750, and 8.5% of his income is roughly $460, he would receive a subsidy of $290, reducing his premium to $460. This represents a significant saving that makes health insurance much more manageable for him as he approaches retirement.

These examples underscore the transformative potential of the ACA 2026 subsidies. They are designed to alleviate financial pressure across various income levels, making quality healthcare a reality for more Americans.

Preparing for Open Enrollment 2026

As 2026 approaches, preparation for open enrollment will be key to taking full advantage of the new ACA 2026 subsidies. Open enrollment typically occurs in the fall of the preceding year, usually starting in November and extending into December or January. Here are essential steps to prepare:

- Stay Informed: Keep an eye on official announcements from HealthCare.gov and your state’s marketplace. Legislative updates regarding the permanent extension or further refinement of subsidies will be crucial.

- Estimate Your 2026 Income: Begin to project your household income for 2026 as accurately as possible. This is the most critical factor in determining your subsidy amount. Factor in any expected raises, job changes, or other income fluctuations.

- Review Your Current Plan: If you currently have an ACA marketplace plan, review its benefits, costs, and network. Even if you like your current plan, new options or changes to your subsidy eligibility might make another plan more beneficial in 2026.

- Explore Plan Options: Don’t just re-enroll in your old plan without checking. New plans enter the market, and existing plans change their offerings annually. The marketplace will display all available plans with your estimated subsidy applied.

- Seek Assistance if Needed: If you find the process confusing, utilize free resources. HealthCare.gov offers a "Find Local Help" tool to connect you with navigators, agents, and brokers who can provide personalized assistance with understanding your options and enrolling.

- Understand Cost-Sharing Reductions (CSRs): In addition to premium tax credits, some individuals with lower incomes may also qualify for Cost-Sharing Reductions (CSRs). These reduce your out-of-pocket costs like deductibles, co-pays, and co-insurance. CSRs are only available with Silver plans, so if you qualify, consider choosing a Silver plan to maximize your overall savings.

By proactively preparing for open enrollment, you can ensure that you secure the best possible health insurance coverage at the most affordable price, fully leveraging the benefits of the ACA 2026 subsidies.

Conclusion: A Brighter Future for Affordable Healthcare

The Affordable Care Act has been a transformative piece of legislation, and its evolution continues with the promising enhancements slated for 2026. The new and extended subsidies represent a significant step towards achieving truly universal and affordable healthcare in the United States. By potentially reducing premiums by up to 25% for many eligible individuals and families, these changes will alleviate financial stress, expand access to care, and ultimately lead to a healthier nation.

Understanding the intricacies of the ACA 2026 subsidies, knowing your eligibility, and actively engaging with the marketplace during open enrollment are crucial steps to harnessing these benefits. The future of healthcare affordability looks brighter, and with these updates, millions more Americans can look forward to securing the vital health coverage they need without compromising their financial well-being. Stay informed, prepare early, and embrace the opportunity to make healthcare more affordable for yourself and your loved ones.