2026 Social Security COLA: Projected 3% Increase and Your Financial Future

Anúncios

In the intricate world of retirement planning, few announcements carry as much weight for beneficiaries as the annual Social Security Cost-of-Living Adjustment (COLA). As we look ahead, projections for the 2026 COLA Projection are beginning to emerge, with a notable 3% increase currently on the horizon. This potential adjustment is more than just a number; it represents a critical lifeline designed to help millions of Americans maintain their purchasing power in the face of inflation. Understanding the nuances of this projection, its calculation, and its potential impact on your financial future is paramount for retirees, those nearing retirement, and anyone concerned about the long-term stability of their Social Security benefits.

Anúncios

The Social Security Administration (SSA) implements the COLA annually to ensure that the value of benefits does not erode due to rising costs of goods and services. Without these adjustments, the fixed income of retirees would steadily decline in real terms, making it increasingly difficult to afford necessities. While the final COLA for 2026 won’t be officially announced until October 2025, early forecasts and economic indicators provide valuable insights into what beneficiaries can expect. A 3% increase, if realized, would reflect ongoing inflationary pressures and the SSA’s commitment to protecting the financial well-being of its recipients. This article will delve deep into the mechanics of the COLA, explore the factors influencing the 2026 COLA Projection, and offer actionable strategies for navigating its implications.

Understanding the Cost-of-Living Adjustment (COLA)

At its core, the COLA is a mechanism designed to counteract inflation. It ensures that the purchasing power of Social Security and Supplemental Security Income (SSI) benefits remains relatively stable over time. The concept is straightforward: as prices for everyday goods and services increase, so too should the benefits received by retirees and other beneficiaries. This adjustment is not arbitrary; it is tied directly to a specific economic index.

Anúncios

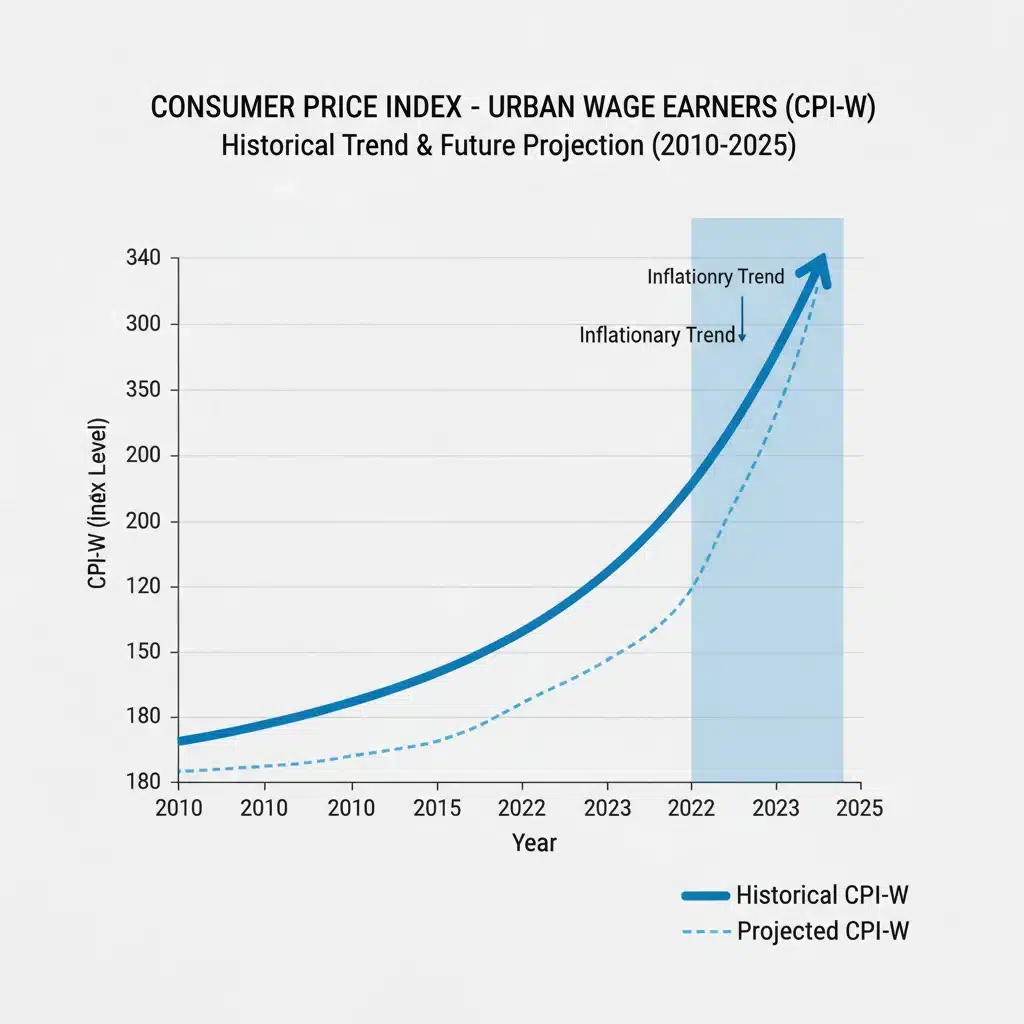

How COLA is Calculated: The CPI-W

The Social Security Administration determines the COLA based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services. This market basket includes everything from food and housing to transportation and medical care.

Specifically, the COLA is calculated by comparing the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the most recent year in which a COLA was payable. The percentage increase between these two periods, rounded to the nearest tenth of a percent, becomes the COLA for the following year. If there is no increase, or if the CPI-W decreases, there is no COLA payment for that year.

It’s important to differentiate the CPI-W from the more commonly cited Consumer Price Index for All Urban Consumers (CPI-U). While both measure inflation, the CPI-W focuses on a subset of the population whose spending patterns may differ from the broader urban consumer group. This distinction is crucial because it directly influences the COLA calculation and, consequently, the benefits received by millions.

Historical COLA Trends and Their Significance

Looking back at historical COLA figures reveals a fascinating pattern of economic shifts. Some years have seen substantial increases, reflecting periods of high inflation, while others have witnessed minimal or even no adjustments. For example, in the early 1980s, COLA increases were in the double digits due to rampant inflation. More recently, there have been years with very low or zero COLA, particularly during periods of economic stagnation or low inflation.

These trends highlight the dynamic nature of inflation and its direct correlation with Social Security benefits. A higher COLA can provide a much-needed boost to beneficiaries’ budgets, helping them keep pace with rising living costs. Conversely, a low or zero COLA can strain finances, especially for those on fixed incomes with limited other sources of retirement income. The 2026 COLA Projection of 3%, therefore, needs to be viewed within this historical context, understanding that it reflects current economic forecasts and the ongoing battle against inflationary pressures.

The 2026 COLA Projection: A Closer Look at 3%

The projection of a 3% COLA for 2026 is a significant figure that warrants detailed examination. While still an estimate, it provides beneficiaries with an early indication of what they might expect in terms of increased Social Security payments. This projection is typically derived from various economic models and forecasts that analyze anticipated inflation rates, particularly those impacting the CPI-W.

Factors Influencing the 3% Projection

Several key economic indicators and trends contribute to the projected 3% COLA for 2026:

- Ongoing Inflationary Pressures: Despite efforts to curb inflation, many economists predict that price increases will continue, albeit at a slower pace than peak levels. Factors such as supply chain disruptions, geopolitical events, and robust consumer demand can all contribute to sustained upward pressure on prices.

- Wage Growth: Strong wage growth can be both a cause and effect of inflation. As wages increase, so does consumer spending power, which can drive up demand and, consequently, prices. This cycle directly impacts the CPI-W, as it reflects the spending habits of urban wage earners.

- Energy Prices: Fluctuations in oil and gas prices have a profound impact on overall inflation. Higher energy costs translate into increased transportation expenses for businesses and consumers, which are then passed on through higher prices for goods and services.

- Housing Costs: Housing, including rent and homeownership costs, is a significant component of the CPI-W. Continued increases in housing expenses can significantly influence the overall inflation rate and, by extension, the COLA.

- Medical Care Costs: Healthcare expenses have historically been a persistent source of inflation. As these costs continue to rise, they exert upward pressure on the CPI-W and future COLA adjustments.

Economic analysts closely monitor these and other factors to refine their COLA predictions. The 3% projection for the 2026 COLA Projection suggests that these underlying inflationary forces are expected to persist, necessitating a substantial adjustment to Social Security benefits.

How a 3% COLA Translates to Your Benefits

A 3% COLA means that if your current monthly Social Security benefit is, for example, $1,800, it would increase by $54 (3% of $1,800), bringing your new monthly benefit to $1,854. While this might seem like a modest increase on a monthly basis, it can add up significantly over a year, providing an extra $648 in annual income.

It’s crucial to remember that this increase applies to your gross benefit amount. Any deductions, such as Medicare Part B premiums, will be applied after the COLA. Therefore, your net increase might be slightly less than the calculated 3% if your Medicare premiums also rise. However, the ‘hold harmless’ provision typically prevents Medicare Part B premiums from increasing by more than the dollar amount of a retiree’s Social Security COLA, ensuring that most beneficiaries do not see a decrease in their net Social Security check due to Medicare premium increases.

Implications of the 2026 COLA for Retirees

The projected 2026 COLA Projection of 3% carries significant implications for current and future Social Security beneficiaries. It can influence various aspects of their financial planning and overall well-being.

Maintaining Purchasing Power

The primary benefit of a COLA is its role in helping retirees maintain their purchasing power. A 3% increase suggests that the cost of living is expected to rise by a similar margin. Without this adjustment, retirees would find their fixed incomes buying less and less each year, eroding their standard of living. The COLA acts as a vital shield against the corrosive effects of inflation, allowing beneficiaries to keep pace with the rising costs of groceries, utilities, healthcare, and other essential expenses.

Impact on Medicare Premiums and Other Deductions

As mentioned, Medicare Part B premiums are often deducted directly from Social Security benefits. While the ‘hold harmless’ provision generally protects most beneficiaries from a net decrease, a higher COLA can sometimes be accompanied by an increase in Medicare premiums. It’s essential for retirees to factor in potential adjustments to these deductions when calculating their actual net benefit increase. Furthermore, other deductions, such as income tax withholding or garnishments, will also be applied to the new, higher gross benefit amount.

Financial Planning and Budgeting Adjustments

For retirees, a projected 3% COLA provides an opportunity to revisit and adjust their financial plans and budgets. This increase can offer a bit more flexibility, whether it’s for covering unexpected expenses, allocating more towards discretionary spending, or simply offsetting the rising costs of living. It’s an opportune moment to review monthly expenditures, assess where the additional funds can be best utilized, and ensure that the budget remains aligned with financial goals.

Considerations for Future Retirees

For those still working and planning for retirement, the 2026 COLA Projection underscores the importance of understanding how Social Security benefits are adjusted over time. It highlights that future benefits will likely continue to be influenced by inflation. This knowledge can inform retirement savings strategies, emphasizing the need for diversified investments that can also grow to combat inflation, rather than solely relying on Social Security adjustments.

Strategies for Navigating Inflation and Maximizing Benefits

Regardless of the specific COLA percentage, inflation remains a persistent challenge for retirees. Proactive financial planning and strategic decision-making are crucial to maximizing benefits and ensuring a secure retirement. The 2026 COLA Projection serves as a timely reminder to review and refine your approach.

Diversifying Retirement Income Streams

Reliance solely on Social Security, even with COLA adjustments, can be risky. Diversifying retirement income streams is paramount. This can include:

- Personal Savings and Investments: Building a robust portfolio of stocks, bonds, and other assets can provide additional income and growth potential, helping to outpace inflation.

- Pensions: If you are fortunate enough to have a pension, understand its inflation-adjustment features.

- Part-time Work: Many retirees choose to work part-time to supplement their income, providing both financial benefits and social engagement.

- Annuities: Certain types of annuities can provide a guaranteed income stream for life, offering a predictable source of funds.

Effective Budgeting and Expense Management

A well-structured budget is a retiree’s best friend. Regularly reviewing expenses, identifying areas for potential savings, and sticking to a spending plan can significantly impact financial stability. Even with a 3% COLA, managing expenses wisely ensures that the increased benefit goes further. Consider:

- Tracking Expenses: Use budgeting apps or spreadsheets to monitor where your money is going.

- Cutting Non-Essential Spending: Identify areas where you can reduce discretionary spending without significantly impacting your quality of life.

- Seeking Discounts and Senior Benefits: Take advantage of senior discounts, loyalty programs, and other benefits that can help reduce costs.

- Optimizing Housing Costs: Consider options like downsizing, relocating to a lower cost-of-living area, or paying off your mortgage to reduce housing expenses.

Healthcare Cost Management

Healthcare is often one of the largest expenses for retirees. Proactive management of these costs is vital:

- Understanding Medicare Options: Carefully evaluate Medicare Advantage plans (Part C) and Medigap policies to find coverage that meets your needs and budget.

- Prescription Drug Savings: Explore generic alternatives, prescription assistance programs, and bulk purchasing options to reduce medication costs.

- Preventative Care: Staying healthy through preventative care can reduce the need for costly treatments down the line.

Staying Informed About Social Security Changes

The Social Security landscape is dynamic. Staying informed about potential legislative changes, benefit adjustments, and program updates is crucial. The official announcement of the 2026 COLA Projection in October 2025 will be a key date, but it’s important to keep abreast of economic forecasts and expert analyses throughout the year.

The Broader Economic Context and Future Outlook

The 2026 COLA Projection does not exist in a vacuum; it is a direct reflection of the broader economic environment. Understanding this context is essential for a comprehensive view of its implications.

Global Economic Trends

Global economic trends, such as international trade, geopolitical stability, and global supply chains, can significantly influence domestic inflation. Events far from home can impact the cost of goods and services in the U.S., directly affecting the CPI-W and, consequently, the COLA. As economies become increasingly interconnected, these global factors play an ever-larger role in local financial realities.

Government Fiscal and Monetary Policies

The actions of central banks, like the Federal Reserve, and government fiscal policies (taxation and spending) have a profound impact on inflation. Interest rate adjustments, quantitative easing or tightening, and government stimulus packages can all influence the rate at which prices change. These policies are constantly evolving, and their effects ripple through the economy, ultimately influencing the COLA calculations.

Long-Term Sustainability of Social Security

While the COLA ensures that current benefits keep pace with inflation, concerns about the long-term sustainability of the Social Security program persist. Debates about potential reforms, such as adjusting the full retirement age, altering the COLA formula, or increasing payroll taxes, are ongoing. While these discussions don’t directly impact the immediate 2026 COLA Projection, they are crucial for understanding the future trajectory of the program and its ability to continue providing inflation-adjusted benefits for generations to come. Beneficiaries and future retirees should stay informed about these policy discussions, as they could shape the future of their retirement security.

Preparing for the Official 2026 COLA Announcement

While the 3% projection for the 2026 COLA Projection offers a valuable preview, it’s vital to remember that it is not the final figure. The official announcement will come in October 2025, after the Social Security Administration has collected and analyzed the CPI-W data for the third quarter of that year. Until then, the projection can fluctuate based on ongoing economic developments.

What to Expect in October 2025

In mid-October 2025, the Social Security Administration will announce the official COLA for 2026. This announcement will detail the exact percentage increase, which will then be applied to benefits starting in January 2026. Beneficiaries will typically receive a letter or notification from the SSA outlining their new benefit amount. It’s a good practice to review this notification carefully to ensure accuracy and understand the precise impact on your monthly income.

Monitoring Economic Indicators

For those who wish to track the potential COLA more closely, monitoring key economic indicators throughout 2025 can provide insights. Pay attention to reports on inflation, particularly those related to consumer prices, energy costs, and housing. Various financial news outlets and government agencies, such as the Bureau of Labor Statistics, regularly publish these reports. While not directly tied to the CPI-W, broader inflation trends can offer clues about the likely direction of the COLA.

Consulting Financial Advisors

For personalized guidance on how the 2026 COLA Projection and broader economic trends might impact your specific financial situation, consulting a qualified financial advisor is highly recommended. A financial professional can help you:

- Assess your current retirement plan and identify any gaps or areas for improvement.

- Develop strategies to mitigate the effects of inflation on your income and savings.

- Optimize your investment portfolio to align with your retirement goals and risk tolerance.

- Understand the interplay between Social Security benefits, Medicare premiums, and other retirement income sources.

Their expertise can be invaluable in ensuring that your retirement strategy is robust and resilient to economic fluctuations.

Conclusion

The projected 3% 2026 COLA Projection is a significant piece of information for millions of Americans who rely on Social Security benefits. It underscores the ongoing challenge of inflation and the importance of the COLA mechanism in preserving the purchasing power of retirees. While the final figure will only be confirmed in October 2025, this early estimate provides a valuable opportunity for proactive financial planning.

By understanding how COLA is calculated, the factors influencing its projection, and its implications for personal finances, beneficiaries can better prepare for the future. Diversifying income streams, practicing effective budgeting, managing healthcare costs, and staying informed about economic trends are all crucial strategies for navigating the complexities of retirement in an ever-changing economic landscape. The goal is not just to receive an adjustment but to ensure that your Social Security benefits, combined with other financial resources, continue to provide a stable and comfortable retirement for years to come. The 2026 COLA Projection is a reminder that vigilance and thoughtful planning are always your best allies in securing your financial future.