Federal Tax Code Changes 2026: Impact on Middle-Class Households

Anúncios

Understanding the Federal Tax Code Revisions in Q1 2026: A Deep Dive for Middle-Class Households

The landscape of federal taxation is perpetually shifting, and the impending changes slated for Q1 2026 are poised to bring about significant transformations. These Federal Tax Code Revisions are not merely minor tweaks; they represent a substantial overhaul expected to directly impact an estimated 70% of middle-class households across the nation. For many, this will necessitate a thorough re-evaluation of personal financial strategies, investment decisions, and even long-term retirement planning. Understanding the nuances of these changes is paramount for individuals and families to navigate the evolving financial environment effectively.

The purpose of this comprehensive guide is to demystify the upcoming legislation, providing a clear and actionable understanding of what these Federal Tax Code Revisions entail. We will delve into the proposed changes, analyze their potential effects on various income brackets within the middle class, and offer expert insights on how to prepare for and adapt to the new tax reality. From adjustments to tax brackets and deductions to implications for specific financial instruments, this article aims to be your definitive resource for understanding the 2026 tax overhaul.

Anúncios

The Genesis of Change: Why These Federal Tax Code Revisions Now?

Tax legislation is rarely static. It evolves in response to economic conditions, political priorities, and societal needs. The Federal Tax Code Revisions scheduled for Q1 2026 are no exception. While the specific legislative drivers are complex and multi-faceted, they generally stem from a combination of factors including:

- Economic Stimulus and Stability: Governments often use tax policy as a tool to stimulate economic growth, manage inflation, or stabilize the economy during periods of uncertainty. The 2026 revisions may be designed to address current or anticipated economic challenges.

- Budgetary Needs: Federal budgets are constantly under review, and tax revenue plays a critical role in funding government programs and services. Revisions can be a way to address budgetary shortfalls or allocate resources more effectively.

- Social and Equity Goals: Tax codes can be designed to promote certain social behaviors (e.g., saving for retirement, charitable giving) or to address income inequality. Some aspects of the 2026 revisions might aim to achieve greater fairness or support specific demographic groups.

- Expiration of Previous Legislation: Many tax provisions have sunset clauses, meaning they are set to expire on a specific date unless reauthorized or modified. A significant portion of the upcoming changes may be a direct result of the expiration of provisions from earlier tax acts, necessitating new legislation to fill the void. This often leads to broad-ranging adjustments rather than minor alterations.

Understanding these underlying motivations can provide valuable context for the specific changes being proposed. It helps to frame the discussion and allows for a more informed analysis of the potential impacts on middle-class households. Without this context, the revisions might appear arbitrary, but they are almost always a reflection of broader governmental objectives.

Anúncios

Key Areas of Impact: What the Federal Tax Code Revisions Mean for Middle-Class Households

The term "middle class" itself can be fluid, but generally encompasses a broad spectrum of income levels and lifestyles. The upcoming Federal Tax Code Revisions are expected to touch upon several critical areas that directly affect this demographic. Let’s break down the most anticipated changes:

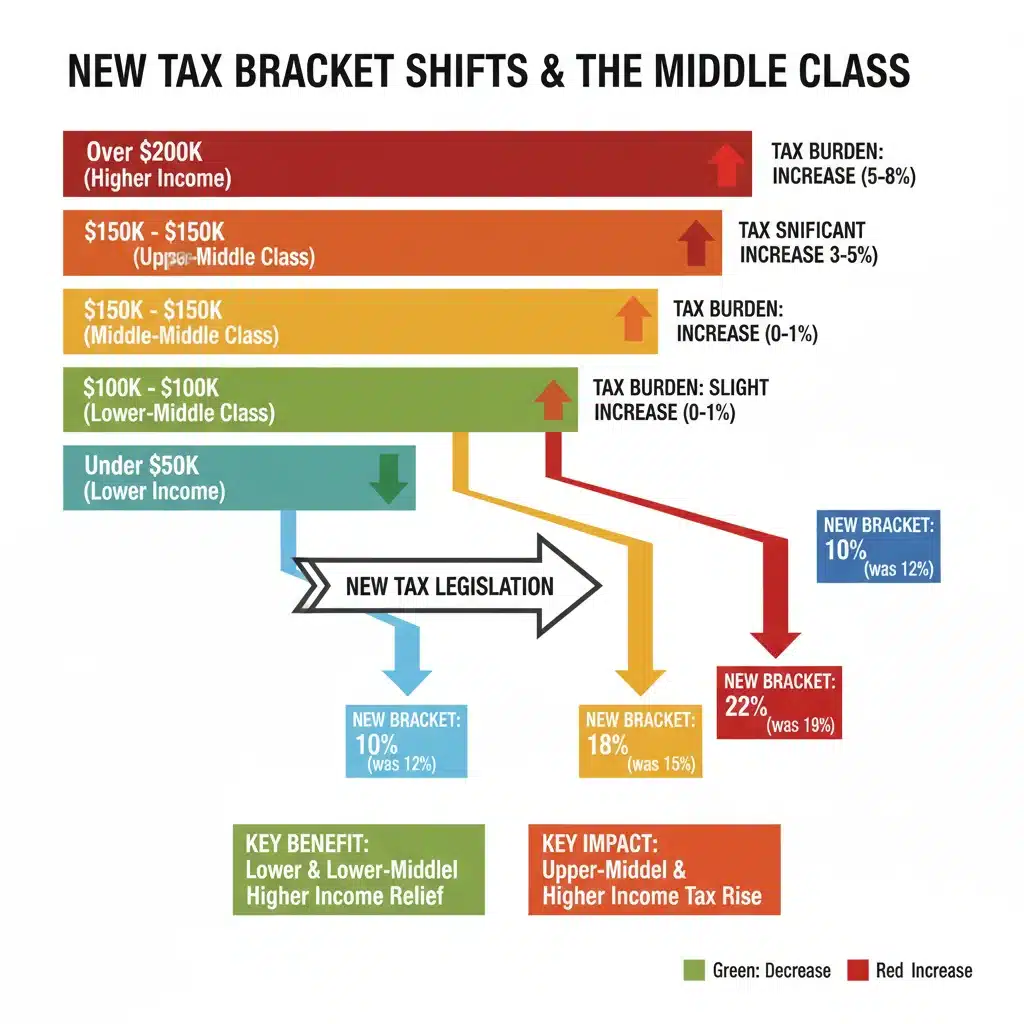

1. Adjustments to Income Tax Brackets and Rates

One of the most direct ways tax legislation impacts individuals is through changes to income tax brackets and rates. While specific figures are still subject to final legislative approval, early indications suggest potential shifts that could either increase or decrease the tax burden for various segments of the middle class. This might involve:

- New Bracket Thresholds: The income ranges defining each tax bracket could be adjusted, potentially moving some households into higher or lower brackets even if their income remains the same.

- Rate Changes: The percentage of income taxed within each bracket might be altered. Even a small percentage change can have a substantial impact on disposable income.

- Inflation Adjustments: Historically, tax brackets are adjusted for inflation. The upcoming revisions might refine how these adjustments are calculated, affecting long-term tax liabilities.

For a middle-class household, understanding where their income falls within the new proposed brackets is crucial. A slight shift could mean hundreds or even thousands of dollars more or less in taxes owed annually. This directly influences budgeting, saving potential, and overall financial stability. It’s not just about the top tax rate, but how the entire progressive system is structured.

2. Changes to Standard Deductions and Itemized Deductions

Deductions play a significant role in reducing taxable income. The Federal Tax Code Revisions are expected to revisit both the standard deduction and various itemized deductions. This could have a profound effect on how many middle-class taxpayers choose to file:

- Standard Deduction Modifications: An increase in the standard deduction could benefit many middle-class households, simplifying tax filing and potentially reducing their taxable income without needing to itemize. Conversely, a decrease could push more taxpayers towards itemizing.

- Itemized Deduction Limitations or Expansions: Deductions for mortgage interest, state and local taxes (SALT), charitable contributions, and medical expenses are often areas of legislative focus. New caps, phase-outs, or even expansions of these deductions could significantly alter the tax benefits available to homeowners, those in high-tax states, or individuals with substantial medical costs.

The interplay between the standard and itemized deductions is vital. Many middle-class families currently find themselves on the cusp, where a slight change in either could dictate their filing strategy and ultimately, their tax liability. It’s essential to analyze which approach will yield the most favorable outcome under the new rules.

3. Impact on Child Tax Credits and Family Benefits

For families, particularly those with children, tax credits can provide substantial financial relief. The 2026 Federal Tax Code Revisions are likely to address these provisions:

- Child Tax Credit (CTC) Adjustments: The amount of the credit, its refundability, and the income thresholds for eligibility are all subject to change. An expansion could provide significant relief, while a contraction could strain family budgets.

- Dependent Care Credits: Changes to credits related to childcare expenses could affect working parents.

- Education-Related Tax Benefits: Credits and deductions for higher education expenses, such as the American Opportunity Tax Credit or Lifetime Learning Credit, may also see revisions, impacting families saving for or currently funding college.

These family-focused provisions directly impact the disposable income and financial planning for millions of middle-class households. Any alteration will necessitate a review of family budgets and future educational or childcare funding plans.

4. Retirement Savings and Investment Implications

The Federal Tax Code Revisions often include provisions that influence how individuals save for retirement and invest their money. Middle-class households rely heavily on tax-advantaged accounts like 401(k)s and IRAs for their future security. Potential changes include:

- Contribution Limits: While typically adjusted for inflation, legislative changes could introduce additional modifications to annual contribution limits for various retirement accounts.

- Tax Treatment of Retirement Distributions: Alterations to how retirement withdrawals are taxed, especially for different account types (e.g., traditional vs. Roth), could influence retirement planning strategies.

- Capital Gains Tax: Changes to the tax rates on long-term capital gains and qualified dividends could affect investment decisions and the overall returns for those with taxable investment accounts.

- Estate Tax Thresholds: While primarily impacting wealthier individuals, changes to estate tax exemptions can sometimes have broader implications or signal a shift in overall tax philosophy that could eventually trickle down.

For middle-class individuals striving to build a secure retirement, these changes could affect the effectiveness of their current savings strategies and necessitate adjustments to their investment portfolios. It’s crucial to stay informed to ensure your long-term financial goals remain on track.

5. Business and Self-Employment Tax Considerations

A significant portion of the middle class engages in self-employment, owns small businesses, or has side hustles. The Federal Tax Code Revisions could also bring changes relevant to these individuals:

- Pass-Through Business Deductions: The Section 199A qualified business income (QBI) deduction, which benefits many pass-through entities, is set to expire. Its reauthorization or modification will be critical for many small business owners.

- Self-Employment Tax Rules: While less frequent, adjustments to self-employment tax calculations or deductions could impact independent contractors and freelancers.

- Depreciation Rules: Changes to bonus depreciation or Section 179 expensing could affect small businesses looking to invest in new equipment or assets.

For the entrepreneurial segment of the middle class, these business-related tax changes can have a direct impact on profitability, investment decisions, and the overall viability of their ventures. Staying abreast of these specific provisions is just as important as understanding personal income tax changes.

Preparing for the 2026 Federal Tax Code Revisions: Actionable Steps

Given the breadth and depth of the anticipated Federal Tax Code Revisions, proactive preparation is key. Waiting until the last minute could mean missed opportunities or unnecessary financial strain. Here are actionable steps middle-class households can take now:

1. Review Your Current Financial Situation

Start by gaining a clear understanding of your current income, expenses, deductions, and tax liabilities. Gather your past tax returns (at least the last two to three years) to see historical patterns. This baseline will be invaluable when comparing against the new provisions. Understand your sources of income, your major deductions (mortgage interest, property taxes, charitable giving), and your existing investment portfolio.

2. Stay Informed and Consult Reliable Sources

Tax legislation is complex, and details can change rapidly during the legislative process. Rely on reputable sources such as the IRS website, established financial news outlets, and professional tax organizations for updates. Avoid speculation and focus on confirmed information as it becomes available. Subscribing to financial newsletters or setting up news alerts for "Federal Tax Code Revisions 2026" can be beneficial.

3. Engage with a Qualified Financial Advisor or Tax Professional

This is perhaps the most crucial step. A knowledgeable financial advisor or certified public accountant (CPA) can provide personalized guidance based on your unique financial circumstances. They can help you:

- Project Your Future Tax Liability: Based on proposed changes, they can estimate how your tax bill might change.

- Identify Potential Strategies: They can recommend adjustments to your income, deductions, or investments to minimize the negative impact or maximize benefits from the new rules.

- Optimize Retirement and Investment Plans: Advisors can help you determine if changes are needed to your 401(k), IRA, or other investment accounts to remain tax-efficient.

- Navigate Complex Provisions: For those with self-employment income, complex investments, or significant deductions, a professional can offer clarity and ensure compliance.

The cost of professional advice often pales in comparison to the potential savings or avoidance of costly errors that can result from navigating complex tax law alone.

4. Re-evaluate Your Budget and Savings Goals

If the Federal Tax Code Revisions lead to an increase in your tax burden, you may need to adjust your household budget to accommodate this. Conversely, if you anticipate a tax reduction, you can strategically allocate those extra funds towards savings, debt reduction, or investments. Review your emergency fund, retirement contributions, and other savings goals in light of potential changes to your take-home pay.

5. Consider "Tax Loss Harvesting" or "Tax Gain Harvesting"

Depending on potential changes to capital gains tax rates, some investors might consider accelerating or delaying the realization of gains or losses. If capital gains rates are expected to rise significantly, realizing gains in the current tax year might be advantageous. Conversely, if rates are expected to fall, delaying gains could be beneficial. This is a sophisticated strategy best discussed with a financial professional.

6. Review Your Withholding or Estimated Tax Payments

Once the new legislation is finalized, it’s crucial to adjust your W-4 form with your employer or modify your estimated tax payments if you are self-employed. This ensures you are not under-withholding (leading to penalties) or over-withholding (tying up funds unnecessarily). A tax professional can help you calculate the correct amounts.

7. Educate Yourself on Specific Industry Impacts

Certain industries or professions within the middle class might be disproportionately affected by specific Federal Tax Code Revisions. For example, changes to clean energy credits might impact those in renewable energy, or modifications to educational deductions could affect teachers or students. Researching industry-specific implications can provide a more tailored understanding.

Long-Term Implications and Future Outlook

The 2026 Federal Tax Code Revisions are not just a one-time event; they are part of an ongoing evolution of tax policy. For middle-class households, these changes underscore the importance of continuous financial vigilance and adaptability. The long-term implications could include:

- Shifts in Economic Behavior: Tax incentives and disincentives can influence decisions about saving, investing, working, and even where people choose to live.

- Impact on Wealth Accumulation: The ability of middle-class families to build wealth over time is directly tied to their disposable income and the tax treatment of their investments and savings.

- Increased Complexity or Simplification: Depending on the nature of the revisions, the tax code could become either more streamlined or more intricate, affecting the ease of compliance for average taxpayers.

It’s important to remember that tax laws are rarely permanent. Future administrations and legislative bodies will undoubtedly introduce further changes. Therefore, developing a habit of staying informed and regularly reviewing your financial plan with a professional will be a continuous necessity for maintaining financial health in a dynamic tax environment.

Conclusion: Navigating the New Tax Horizon

The impending Federal Tax Code Revisions in Q1 2026 represent a critical juncture for 70% of middle-class households. While the specifics are still being finalized, the potential for widespread impact on income, deductions, and financial planning strategies is undeniable. From adjustments to tax brackets and standard deductions to changes in family credits and investment rules, every aspect of personal finance could see significant shifts.

Rather than viewing these changes with apprehension, middle-class households should see them as an impetus for proactive engagement. By understanding the potential impacts, staying informed through reliable sources, and most importantly, consulting with qualified financial and tax professionals, you can effectively navigate this new tax horizon. Strategic planning now can minimize adverse effects and even uncover new opportunities for financial optimization. The goal is not just to comply with the new rules, but to thrive within them, ensuring your financial future remains secure and prosperous.