Student Loan Forgiveness 2026: Navigating the 3-Month Application Window

Anúncios

Student Loan Forgiveness 2026: Navigating the 3-Month Application Window

The landscape of student loan debt in the United States is constantly evolving, with millions of Americans grappling with the financial burden of higher education. As we approach 2026, a critical 3-month application window for various student loan forgiveness programs is anticipated, offering a beacon of hope for many. Understanding the intricacies of these programs, eligibility requirements, and the precise timing of this window will be paramount for borrowers seeking relief. This comprehensive guide aims to demystify the process, providing actionable insights and essential information to help you prepare for and successfully navigate the upcoming opportunities for student loan forgiveness 2026.

Anúncios

The promise of student loan forgiveness has been a significant topic of discussion and policy debate for years. While broad, sweeping forgiveness has faced legal and political hurdles, targeted programs continue to provide relief to specific groups of borrowers. The year 2026 is shaping up to be a pivotal moment, with a concentrated application period that could determine the financial future for countless individuals. This article will delve into the current state of student loan forgiveness, highlight the programs expected to be active, and provide a step-by-step roadmap for preparing your application.

Understanding the Current Landscape of Student Loan Forgiveness

Before we dive into the specifics of student loan forgiveness 2026 and the 3-month application window, it’s crucial to grasp the current environment of student debt relief. The past few years have seen significant shifts, including payment pauses, interest waivers, and the implementation of new or expanded forgiveness initiatives. These changes often lead to confusion, making it vital for borrowers to stay informed.

Anúncios

Recent Developments and Policy Changes

The federal government has made several attempts to address the student loan crisis. While some large-scale forgiveness plans have been challenged in courts, other administrative actions have successfully provided relief. For example, adjustments to income-driven repayment (IDR) plans have led to forgiveness for borrowers who have made payments for 20 or 25 years. The Public Service Loan Forgiveness (PSLF) program has also seen significant improvements, making it more accessible to eligible public servants. These ongoing efforts underscore a continued commitment to providing relief, albeit through more targeted mechanisms.

The Importance of Staying Informed

The rules and regulations surrounding student loan forgiveness can change rapidly. What was true last year might not be true next year. Therefore, regularly checking official sources, such as the U.S. Department of Education’s Federal Student Aid (FSA) website, is essential. Subscribing to newsletters and following reputable financial news outlets can also help you stay abreast of any new developments that could impact your eligibility for student loan forgiveness 2026.

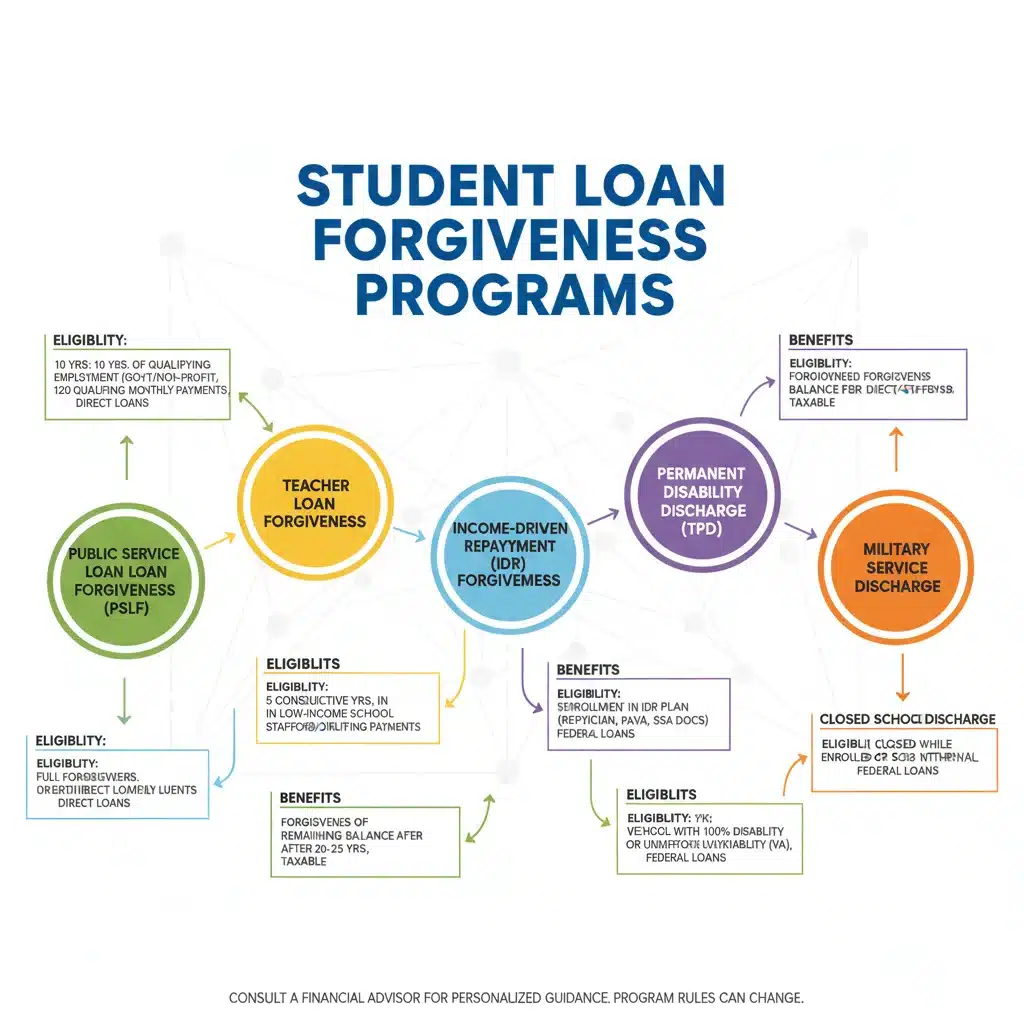

Key Programs Expected to Offer Forgiveness in 2026

The anticipated 3-month application window in 2026 will likely focus on specific, established programs that have undergone recent enhancements or are slated for renewed attention. While predicting exact program details so far in advance can be challenging, several key initiatives are expected to play a significant role. Understanding these programs is the first step toward preparing your application.

Public Service Loan Forgiveness (PSLF)

The PSLF program is designed to forgive the remaining balance on Direct Loans after 120 qualifying monthly payments have been made under a qualifying repayment plan while working full-time for a qualifying employer. Qualifying employers include government organizations (federal, state, local, or tribal) and not-for-profit organizations. Recent temporary waivers have made it easier for past payments, even those made under non-qualifying plans, to count towards the 120 payments. It is highly probable that PSLF will be a cornerstone of student loan forgiveness 2026 efforts, especially for those who have been working in public service for an extended period.

Eligibility for PSLF

- Loan Type: Only Direct Loans qualify. Other federal loans may become eligible after consolidation into a Direct Consolidation Loan.

- Employment: Full-time employment with a U.S. federal, state, local, or tribal government or a not-for-profit organization.

- Payments: 120 qualifying monthly payments (not necessarily consecutive) made under a qualifying repayment plan.

Income-Driven Repayment (IDR) Plan Forgiveness

IDR plans are designed to make student loan payments more manageable by capping them at a percentage of your discretionary income. After 20 or 25 years of payments (depending on the plan and when you borrowed), any remaining balance on your federal student loans is forgiven. Recent administrative actions have aimed to correct historical inaccuracies in payment tracking, leading to many borrowers receiving forgiveness through IDR plans sooner than expected. This trend is expected to continue into 2026, making IDR forgiveness a crucial component of the upcoming application window.

Types of IDR Plans

- Revised Pay As You Earn (REPAYE) Plan: Generally 10% of discretionary income.

- Pay As You Earn (PAYE) Plan: Generally 10% of discretionary income.

- Income-Based Repayment (IBR) Plan: Generally 10% or 15% of discretionary income.

- Income-Contingent Repayment (ICR) Plan: The lesser of 20% of discretionary income or what you’d pay on a fixed 12-year payment plan.

- Saving on a Valuable Education (SAVE) Plan: A newer, more generous IDR plan designed to significantly reduce monthly payments and offer faster forgiveness for some borrowers. The SAVE plan is expected to be a major pathway for student loan forgiveness 2026.

Total and Permanent Disability (TPD) Discharge

Borrowers who are determined to be totally and permanently disabled may be eligible to have their federal student loans discharged. This relief is typically granted through an application process that involves documentation from a physician, the Social Security Administration (SSA), or the Department of Veterans Affairs (VA). While not tied to a specific application window in the same way as PSLF or IDR, ongoing administrative reviews and automatic discharges for certain TPD recipients mean that this remains an important avenue for relief that could be highlighted during the 2026 period.

Teacher Loan Forgiveness (TLF)

Teachers who work for five complete and consecutive academic years in a low-income school or educational service agency may be eligible for forgiveness of up to $17,500 on their Direct Subsidized and Unsubsidized Loans and their Subsidized and Unsubsidized Federal Stafford Loans. This program operates independently of the broader forgiveness initiatives but is a consistent source of relief for educators and may be a focus during the 2026 window for eligible applicants.

Preparing for the 3-Month Application Window in 2026

The announcement of a specific 3-month application window for student loan forgiveness 2026 signifies a focused period of opportunity. Proactive preparation will be key to maximizing your chances of successful forgiveness. This involves several critical steps, from understanding your loan types to gathering necessary documentation.

Step 1: Understand Your Loan Types

Not all student loans are eligible for all forgiveness programs. Federal student loans are generally the only ones that qualify for federal forgiveness programs. Private student loans, issued by banks or other financial institutions, typically do not qualify for federal forgiveness. You can find information about your federal student loans by logging into your account on the Federal Student Aid (FSA) website (StudentAid.gov).

- Direct Loans: Most federal loans issued since 2010 are Direct Loans and are generally eligible for all federal forgiveness programs.

- FFEL Program Loans: Federal Family Education Loan (FFEL) Program loans are older federal loans. Some may require consolidation into a Direct Consolidation Loan to become eligible for certain programs like PSLF or IDR forgiveness.

- Perkins Loans: Federal Perkins Loans may also require consolidation.

It’s crucial to identify your loan types well in advance. If consolidation is necessary, it can take several weeks to process, so starting this process early is advisable.

Step 2: Consolidate Your Loans (If Necessary)

As mentioned, certain older federal loans (FFEL, Perkins) may need to be consolidated into a Direct Consolidation Loan to qualify for PSLF or certain IDR plans. Consolidation combines multiple federal loans into a single new loan with one servicer and one monthly payment. Importantly, consolidation can also allow past payments on ineligible loans to count towards PSLF or IDR forgiveness under specific waivers or adjustments. This could be a game-changer for many borrowers seeking student loan forgiveness 2026.

Considerations for Consolidation:

- Loss of Benefits: Consolidating Perkins Loans or FFEL loans could mean losing some benefits associated with those loans (e.g., cancellation for certain teaching positions under Perkins). Weigh the pros and cons carefully.

- Interest Rate: The interest rate for a Direct Consolidation Loan is the weighted average of the interest rates on the loans being consolidated, rounded up to the nearest one-eighth of one percent.

- Timing: Do not wait until the last minute to consolidate. The process can take 30-90 days.

Step 3: Review and Update Your Income-Driven Repayment (IDR) Plan

If you are pursuing forgiveness through an IDR plan, ensure you are enrolled in the most beneficial plan for your financial situation. The SAVE Plan, for instance, offers lower monthly payments and more generous interest subsidies than older IDR plans for many borrowers. Regularly recertifying your income and family size is essential to keep your payments accurate and on track for forgiveness. Missing recertification deadlines can lead to capitalized interest and higher payments.

Step 4: Document Your Employment for PSLF

For PSLF, meticulous record-keeping is non-negotiable. You must prove your employment with qualifying organizations for 120 months. Use the PSLF Help Tool on StudentAid.gov to generate and submit the PSLF & Temporary Expanded PSLF (TEPSLF) Certification & Application (PSLF Form) annually or whenever you change employers. This ensures your payments are being accurately counted and your employment is verified. Even if you’re not yet at 120 payments, certifying your employment regularly is vital to ensure your path to student loan forgiveness 2026 is clear.

Step 5: Gather Necessary Documentation

Regardless of the specific program, applying for student loan forgiveness will require documentation. Start gathering these items now:

- Financial Records: Income tax returns (Form 1040), pay stubs, and any other proof of income.

- Loan Documents: Promissory notes, statements from your loan servicer, and records of past payments.

- Employment Records: W-2s, employment verification forms, and pay stubs, especially for PSLF.

- Disability Documentation: If applicable, medical records or documentation from the SSA or VA for TPD discharge.

- Identification: Government-issued ID.

Having these documents organized and readily accessible will streamline the application process during the 3-month window.

The 3-Month Application Window: What to Expect

While the exact dates and specific mechanisms of the 3-month application window for student loan forgiveness 2026 are yet to be officially announced, we can anticipate certain characteristics based on past initiatives and current trends.

Anticipated Timing and Communication

The U.S. Department of Education typically provides ample notice for significant application periods. Expect official announcements through StudentAid.gov, emails to borrowers, and press releases. It’s crucial to ensure your contact information with your loan servicer and on StudentAid.gov is up to date so you don’t miss critical communications.

Application Process and Platform

Most federal student loan applications are handled online through the Federal Student Aid website. The application process will likely be user-friendly, guiding borrowers through eligibility questions and document submission. However, given the potential volume of applications, be prepared for possible website slowdowns or extended processing times. Applying early within the window, once it opens, is generally advisable.

Potential Scope of the Window

This 3-month window could be a concentrated effort to process applications for borrowers who have become eligible under recent policy changes (e.g., IDR account adjustments) or to encourage new applications for ongoing programs like PSLF and the SAVE Plan. It might also be an opportunity to address specific cohorts of borrowers or to simplify the application process for certain types of relief. The focus will likely be on ensuring that eligible borrowers, particularly those who have have been making payments for many years or are in public service, receive the forgiveness they are due.

Common Pitfalls and How to Avoid Them

Navigating student loan forgiveness can be complex, and several common mistakes can delay or even derail your application. Being aware of these pitfalls can help you avoid them and ensure a smoother path to student loan forgiveness 2026.

1. Not Knowing Your Loan Type

As emphasized earlier, the type of loan you have is fundamental to eligibility. Many borrowers mistakenly believe all student loans qualify for all programs. Verify your loan types on StudentAid.gov.

2. Missing Deadlines

Whether it’s for consolidation, IDR recertification, or the actual forgiveness application, deadlines are critical. Set reminders and keep a calendar to track important dates.

3. Incomplete or Inaccurate Documentation

Any missing or incorrect information can lead to delays or rejection. Double-check all forms and ensure all required supporting documents are attached and clearly legible.

4. Falling Victim to Scams

Unfortunately, student loan forgiveness is a target for scammers. Be wary of any company that charges a fee for services that are free through the Department of Education, promises guaranteed forgiveness, or pressures you to act immediately. Always go through official channels.

5. Not Certifying Employment for PSLF Regularly

Many PSLF hopefuls wait until they believe they’ve made 120 payments to certify their employment. This can lead to discovering issues with qualifying employment or payments years later. Certify annually!

6. Misunderstanding IDR Recertification

Failing to recertify your income and family size for an IDR plan annually can result in your payments increasing and capitalized interest being added to your loan balance, making forgiveness less impactful.

Beyond Forgiveness: Other Debt Relief Options

While the focus is on student loan forgiveness 2026, it’s important to remember that not everyone will qualify for these programs. If you find that forgiveness isn’t an option for you, other strategies can help manage your student loan debt.

Refinancing Private Student Loans

If you have private student loans or federal loans that don’t qualify for forgiveness, refinancing through a private lender might be an option. This could lead to a lower interest rate or a more manageable monthly payment, but be cautious: refinancing federal loans into private ones means losing access to federal benefits like IDR plans and forgiveness.

Deferment and Forbearance

These options allow you to temporarily postpone or reduce your student loan payments. While they can provide short-term relief during financial hardship, interest may still accrue, potentially increasing your total loan cost. They are not pathways to forgiveness but can be crucial safety nets.

Aggressive Repayment Strategies

For those who don’t qualify for forgiveness and want to pay off their loans faster, strategies like the debt avalanche or debt snowball method can be effective. The debt avalanche prioritizes loans with the highest interest rates, while the debt snowball focuses on paying off the smallest balances first to build momentum.

The Future of Student Loan Forgiveness

The conversation around student loan debt and forgiveness is ongoing. Political and economic factors will continue to influence policy decisions. While the 3-month application window in 2026 offers a specific opportunity, it’s part of a larger, evolving effort to address the student debt crisis. Advocacy groups continue to push for broader relief, and new legislative proposals may emerge.

Borrowers should maintain a proactive stance: stay informed, regularly review their financial situation, and utilize all available resources. The Federal Student Aid website remains the authoritative source for information regarding federal student loan programs. Financial aid counselors and non-profit credit counseling agencies can also provide personalized guidance.

Conclusion

The anticipation of a 3-month application window for student loan forgiveness 2026 offers a significant opportunity for millions of borrowers. By understanding the current landscape, identifying eligible programs like PSLF, IDR plans (especially the SAVE Plan), and TPD discharge, and meticulously preparing your documentation, you can position yourself for success. Proactive engagement with your loan servicer, regular checks of official government websites, and vigilance against scams are crucial steps in this journey.

Student loan debt can be a formidable obstacle, but with careful planning and informed action, the path to financial relief through forgiveness programs becomes clearer. Take the time now to assess your situation, gather your documents, and prepare for this critical window. Your financial future could depend on it.

Frequently Asked Questions (FAQs)

- Q: What exactly is the ‘3-month application window’ for 2026?

- A: While specific details are pending official announcements, this refers to a concentrated period in 2026 where the Department of Education is expected to open or streamline applications for various existing federal student loan forgiveness programs. This could be to process applications under new rules, address specific borrower groups, or encourage wider participation.

- Q: How do I know if my loans are federal or private?

- A: You can find this information by logging into your account on StudentAid.gov. Private loans will not appear on this site. If you have loans from a bank or private lender, they are likely private.

- Q: I have FFEL loans. Will they qualify for forgiveness in 2026?

- A: FFEL loans typically need to be consolidated into a Direct Consolidation Loan to qualify for most federal forgiveness programs like PSLF or IDR forgiveness. It’s highly recommended to consider consolidation well before the 2026 window if you aim for these programs.

- Q: Is there any broad, automatic forgiveness expected in 2026?

- A: While administrative actions continue to provide targeted automatic forgiveness for certain groups (e.g., some IDR borrowers, TPD recipients), broad, universal forgiveness has faced legal challenges. The 2026 window is more likely to focus on existing, enhanced programs requiring an application.

- Q: How can I protect myself from student loan forgiveness scams?

- A: Be skeptical of unsolicited offers. The Department of Education will never charge a fee for forgiveness programs. Always verify information through official sources like StudentAid.gov or your official loan servicer.

- Q: What if I don’t qualify for any forgiveness programs?

- A: If forgiveness isn’t an option, explore other repayment strategies such as enrolling in an Income-Driven Repayment (IDR) plan to lower your monthly payments, or consider deferment or forbearance during periods of financial hardship. For private loans, refinancing might be an option to reduce interest rates.